Do You Have to Pay Tax on Buying and Selling Virtual Currency? | I Earned 10 Billion In-Game Coins—How Much Tax Would I Owe?

Distinguishes between Bitcoin-style cryptocurrencies and game virtual currencies under Chinese tax law, explaining when in-game currency transactions trigger personal income tax obligations and why most casual trading remains practically untaxed.

Previously, rumors circulated that the Shanghai Tax Bureau published an article on its official account titled “Common Misconceptions About Business Income and Categorical Income from Personal Income Tax” (after searching, the article could no longer be found on the “Shanghai Tax” account but remained on the “Xuhui Tax” account), stating that “individuals buying and selling virtual currency online need to pay personal income tax.”

This raised many questions:

Is this official support for “virtual currency” (specifically Bitcoin-like)?

Do game充值 and virtual currency transactions need to be taxed?

If I sell in-game items and make money, do I need to pay tax?

“I” earned 10 billion in-game coins—how much tax would I owe?

*This article represents only the author’s personal views and is not intended as legal advice or opinion.

I. This “Virtual Currency” Is Not That “Virtual Currency”

Although various official accounts only recently sent this article, the content is not news.

As the批复 number cited in the article “Guo Shui Han [2008] No. 818” indicates, this批复 was actually issued in 2008.

(https://www.chinatax.gov.cn/chinatax/n363/c4185/content.html)

(https://www.chinatax.gov.cn/chinatax/n363/c4185/content.html)

At that time, there was still over a month until the release of the first virtual currency Bitcoin whitepaper (October 31, 2008); by May 22, 2010, 10,000 BTC could only buy two pizzas.

In terms of liquidity and value, when the批复 was issued, Bitcoin-led virtual currencies had little value, so the批复 certainly did not refer to them.

On the contrary, the “Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation (Yin Fa [2021] No. 237)” issued in 2021 made it very clear:

(1) Virtual currency does not have the same legal status as legal tender. Bitcoin, Ethereum, Tether, and other virtual currencies have the main characteristics of not being issued by monetary authorities, using encryption technology and distributed accounts or similar technologies, and existing in digital form. They are not legal tender and should not and cannot circulate in the market as currency. (2) Virtual currency-related business activities are illegal financial activities. Engaging in the exchange of legal tender and virtual currency, exchange between virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediation and pricing services for virtual currency transactions, token issuance financing, and virtual currency derivative trading and other virtual currency-related business activities are suspected of illegal issuance of token tickets, unauthorized public issuance of securities, illegal futures trading, illegal fundraising and other illegal financial activities, all of which are strictly prohibited and resolutely banned according to law. If such illegal financial activities constitute a crime, criminal liability will be pursued according to law.

Common virtual currencies like Bitcoin that use encryption technology and distributed accounts have had all their business activities characterized as “illegal financial activities.”

Income from such activities is “illegal gains”

Naturally, there is no so-called “tax payment”

(In reality, it’s more likely to be called “confiscation of illegal gains”?)

II. What Exactly Is This “Virtual Currency”

Since it’s not Bitcoin, what exactly is this “virtual currency”?

In previous articles, we have analyzed what counts as “virtual currency” in the gaming industry (click the link below to view):

Diamonds, Gold Coins, Yuanbao, Coupons… Are Recharged Items Virtual Currency or Game Coins?

The “Notice on Strengthening the Management of Online Game Virtual Currency” (Wen Shi Fa [2009] No. 20) issued in 2009 considered that “virtual currency” only includes “platform currency”:

(1) The online game virtual currency referred to in this notice means a virtual exchange tool issued by online game operating enterprises, purchased directly or indirectly by game users with legal tender at a certain ratio, existing outside the game program, stored on servers provided by the online game operating enterprise in the form of electromagnetic records, and expressed in specific digital units. Online game virtual currency is used to exchange for online game services provided by the issuing enterprise within a specified scope and time, manifested in forms such as prepaid recharge cards, prepaid amounts, or points for online games, but does not include game props obtained during game activities.

It was not until the “Guidelines on the Supervision and Enforcement of Online Game Virtual Currency (Ban Shi Fa [2010] No. 33)” issued in 2010 that game props used for lotteries (game coins) were classified under “virtual currency”:

In the actual regulatory process, virtual props (game coins) directly purchased by users with legal tender and having the function of exchanging for other game props, game coins, or value-added services provided by the game operator may be managed with reference to the management requirements for online game virtual currency.

Back in 2008, although “virtual currency” according to actual regulations mostly referred to “platform currencies” like “Q Coins,” the批复 uses the term “player,” and considering the popularity of games like World of Warcraft, ZT Online, and Legend at that time, there was also a possibility of classifying game coins under “virtual currency.”

Therefore, in 2008, it mainly referred to the act of purchasing “Q Coins” and other virtual currencies (including Q Coin recharge cards) or various game coins from others and reselling them, which required personal income tax.

This indeed aligns with the tax regulations and the “virtual currency” trading market environment of that time.

But considering the tax reporting mechanisms of that era, the total tax revenue collected from the issuance of the批复 to the present

Probably isn’t a large number

III. Do We Still Need to Pay Tax on Trading “Virtual Currency” (“Game Coins”) Now?

Probably yes.

But in practice, it’s more likely difficult to “legally” trade and simply calculate and pay taxes.

1 Game Companies Rarely Allow Trading

Currently, mainstream game companies generally retain ownership of “game accounts” for themselves, with users only having usage rights.

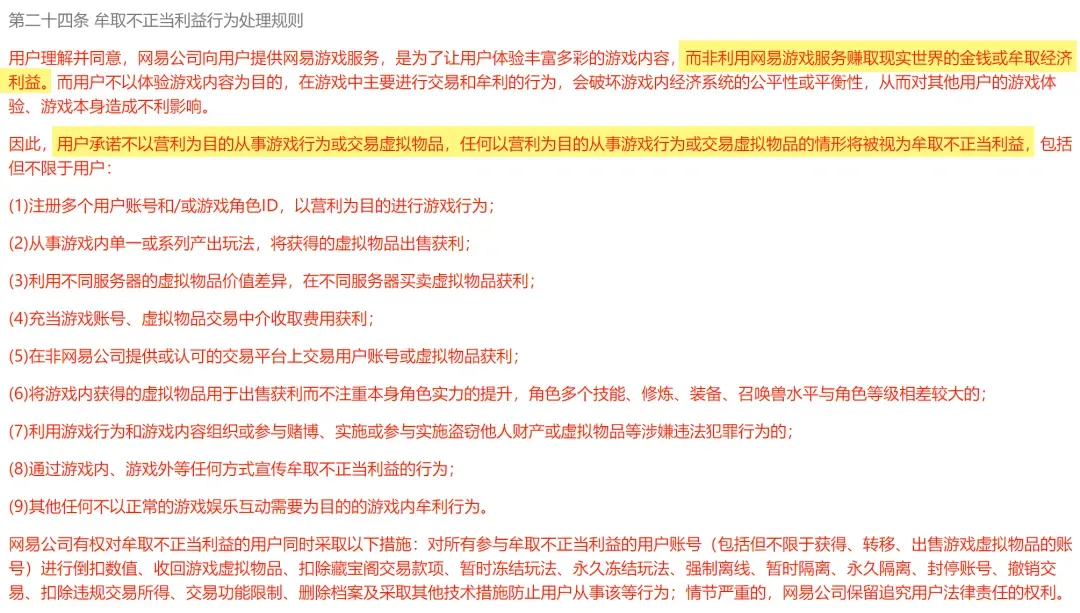

At the same time, they define the trading of “virtual property” as “improper conduct,” such as NetEase Games’ user agreement:

And Tencent Games’ user agreement:

Although there have been multiple cases supporting users’ right to sell props or accounts, such as:

The act of selling game accounts still fundamentally violates the game company’s user agreement.

In the case of Tencent suing Taoshouyou, the Chongqing Pilot Free Trade Zone People’s Court ruled that Guizhi Quzhi Network Technology Co., Ltd.’s Taoshouyou platform, which provided services for “Dungeon & Fighter” game accounts and gold coin transactions, constituted unfair competition, ordering Guizhi Quzhi to cease infringement and compensate Tencent for losses.

Therefore, selling virtual currency for profit without the game company’s permission makes it difficult to directly confirm as legitimate income.

2 Trading Platforms Basically Won’t Withhold Income Tax; If You Do This Professionally, Consider Declaring Voluntarily

Looking at well-known virtual property trading platforms like Jiaoyimao, the user agreements do not mention income tax payment.

According to research, this is not an omission but rather trading platforms do not actually withhold income tax on behalf of users.

Although from the above we know that game companies do not casually allow users to trade virtual currency, the “Civil Code” has already recognized “network virtual property”:

Article 127: Where there are provisions of law regarding the protection of data and network virtual property, those provisions shall apply.

On this basis, combined with the essence of the批复, transferring network virtual property may also be considered as falling under Article 2 of the “Personal Income Tax Law”:

Article 2: The following categories of personal income shall be subject to personal income tax: (1) Income from wages and salaries; (2) Income from remuneration for personal services; (3) Income from author’s remuneration; (4) Income from royalties; (5) Business income; (6) Income from interest, dividends, and bonuses; (7) Income from property leasing; (8) Income from property transfer; (9) Incidental income.

If selling virtual currency is one’s profession, it is business income;

If it’s an occasional transfer of game virtual currency, it is property transfer income.

All of it needs to be taxed.

However, considering that the actual costs (actual money, time, and labor costs) and earnings of users are difficult to calculate, figuring out the tax payable is not easy for ordinary people.

For example, NetEase’s “Cabinet” platform also notes in the user agreement that “all tax obligations… shall be paid by the user themselves”:

But during actual transactions, there are no obvious pop-up windows or other means to remind users to pay taxes or provide tax calculation tools.

Relying entirely on users themselves has resulted in the vast majority of people buying and selling game virtual property being “generally non-compliant.”

Considering that current law does not provide a clear calculation method

The author suggests that ordinary users who can calculate their trading profits should file taxes annually to avoid “tax evasion”

If you are a professional seller, it’s best to accurately calculate your actual earnings and pay taxes according to law to avoid constituting “tax fraud.”

IV. Do You Need to Pay Tax on Game Coins Earned in Games?

Some online games’ virtual currency pricing is essentially tied to reality, for example, XX virtual currency can be exchanged for a monthly card (worth a certain amount of RMB).

So, if you earn virtual currency in the game (through gameplay, not by selling real monthly cards, etc.), do you need to pay tax based on its pricing?

The author believes that no matter how many game coins (or even “virtual currency”) you earn in the game, as long as you do not transfer them to other users and simply spend them again within the game, it does not constitute a taxable event and no tax is required.

The批复 only states that “purchasing virtual currency from other users and then reselling it” constitutes a “taxable event.” Based on the “Personal Income Tax Law,” we can analyze that transferring game virtual property may also constitute a “taxable event.”

But game coins earned within a game are essentially part of the game data and depend on the game for their existence.

Before intersecting with the real world (such as selling or gifting), game coins in games do not have real-world value and are not equivalent to legal tender (nor does the law allow it). Simply put, they have no “taxable” capacity.

If users earn game coins in a game and then reinvest them in the game, it can only be seen as a circulation of electronic data—users enjoying the “gameplay” rather than gaining “income” from the game.

Such behavior cannot constitute any of the circumstances in the “Personal Income Tax Law” and certainly cannot constitute a “taxable event.”

V. Conclusion

The article published by the Shanghai Tax Bureau this time was likely a repost. However, as the first official article to mention “games” (“players”) again after the “Online Game Management Measures (Draft),” it inevitably sparked discussion.

But the批复 was issued in 2008, nearly 16 years ago. The current market environment and actual situation of “virtual currency” are vastly different from back then.

Although the Shanghai Tax Bureau’s original intention may have been legal education, in the current industry environment, any hint of news can spark various discussions.

Perhaps for this reason, the Shanghai Tax Bureau withdrew the article.

Regarding the current reality of game property ownership

There is still a long way to go for virtual property rights and tax law content

Of course

It might be better for tax law to take it slow